Where will digital transformation lead?

Society, companies and connectivity in a brave new world.

Digital transformation is making enormous strides. In this article, we learn how it impacted our life, what companies became successful and what do CSPs need to expect soon.

How many minutes does it take to get to the nearest restaurant? Twenty years ago, we would use a landline phone, a reference book and a map to find an answer. Ten years ago, we would use a browser on a PC. Five years ago, we would surf the Internet on a smartphone to get the answer.

The key thing here is not the change of methods of looking for an answer. It is the response itself that evolved. "Half an hour drive" would be the answer twenty years ago. But now the cinema is inside a PC or a tablet and you can reach it any second simply by running the app.

Limits of digitalization

Books, newspapers, music, video and games have already gone through digitalization. Everything that used to exist on various information media (physical or electronic analog sources) became digital, then it found its way to the Internet and, finally, to users' pockets.

This stage that began with the spread of PCs and the Internet in offices and at home had been completed by the time of 4G introduction and the boom of the smartphone market. The bulk of traditional information has already been digitized by now.

What to digitize further? At first, we could turn to data readings of smart sensors. This is from where the Internet of Things concept comes from. Secondly, it is possible to add information value to huge data stored in various IT systems – from a BSS of a mobile operator to "clicks" done by audiences of online cinemas. For this purpose, we have the Big Data. Thirdly, it is possible to organize the work of traditional businesses via digital interfaces. This is what digital invaders are doing – in other words, performing "uberization" of various businesses.

Is it the time for CSPs to panic?

The idea that CSPs are turning into pipelines which simply deliver someone else's data is appalling. This is strange at first glance, as operators did not generate a significant share of data themselves neither in the age of Voice, nor during the rule of SMS messaging. Calls and messages were coming from people and companies. Then why could operators get a share in data trafficking?

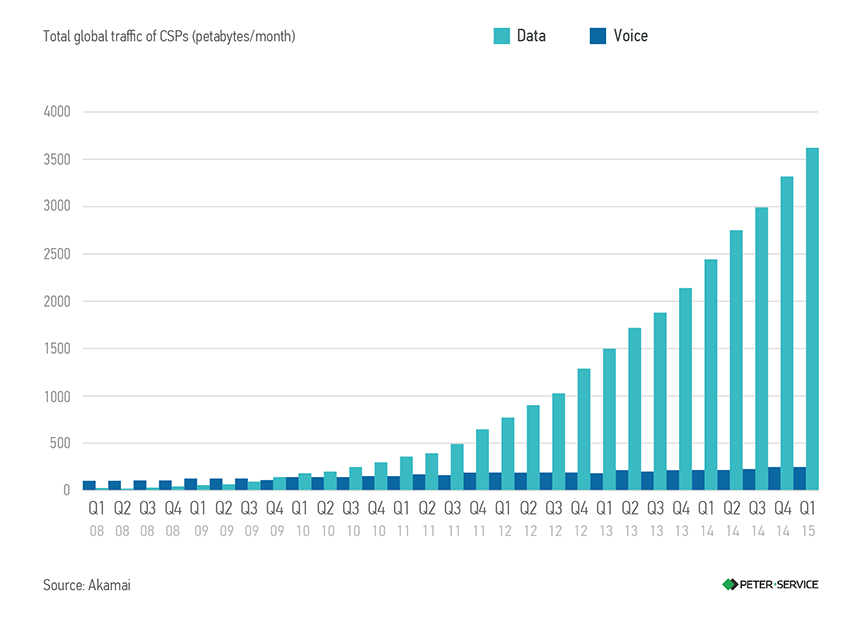

The answer is hidden in detailed statistics. Voice traffic is almost constant; it increases in proportion to the growth of the subscriber base. Data traffic is quite different: it augments almost exponentially per each subscriber year after year.

The reasons are obvious: earlier, subscribers carefully browsed websites anxious not to go negative on their balance by downloading pictures, but today they are confident enough to go beyond consuming pictures and music to streaming clips, films and TV shows (the resolution of these videos can grow almost infinitely).

"If we do move petabytes of data, let those petabytes be ours", this is what operators probably think.

Moreover, the problem is not about traffic volumes, rather than in the possibility to make additional profit from it.

CAPEX vs OPEX

Third companies did not make much on SMS and Voice: they were an additional value for their core business. But in a digital environment companies gained a powerful leverage that led to the appearance of a plethora of rapidly excelling startups that reached success by being present on everyone's phones.

There is an opinion that a digital platform in the form of a handy aggregator app is just the starting point for digital invaders. It is just a way to make first money, acquire the audience and then rush into "digical" (a mix of digital and physical). Such digital platforms as Netflix already produce films on their own and Google is laying optical fiber. Then, there is hardly anything to prevent Uber from acquiring its own smart car fleet or Alibaba from having innovative warehouses equipped with drones, right?

In this respect, the whole story of digital transformation comes down to "good old" wrestling of OPEX and CAPEX in companies' cost structures. Today, OTT companies accumulated enough profits to begin growing CAPEX and reduce OPEX, i. e. to shift to traditional business models, although with a digital dimension.

Catch up and overtake

What about operators? The need to tread a digital path is unquestionable, but to do this, it is necessary to remove everything irrelevant from their business and add lacking components. For example, they can reduce costs of an inefficient BSS and transform it. This will lead to additional CAPEX, but these expenses will help reduce OPEX badly needed to support new digital services.

Only now digital invaders are coming closer to physical infrastructure. CSPs already have it. They just need to digitize it, i.e. to add a digital extension to it. This can be a convenient IoT platform, a good clone of existing OTT services, or a modification of their core telecom business.

Lastly, operators can use the methods, utilized by Netflix to generate new content (based on the analysis of user actions), to improve operational services – urgent deployment of additional base stations, or to profile users and approach them with special offers. The latter can be used to identify travelling subscribers and develop tailored services for them or to find active users of certain types of content, e. g. those addicted to TV shows.

Digital future

Some companies are severely affected by digital invaders. Others are hastily performing digital transformation of their business – from management systems to launching their own digital shop windows.

Yet, without CSPs digital transformation would be impossible. They are the ones providing all digital services with Internet, M2M and, eventually, end users.

CSPs have a chance to win "the digital race". But, first and foremost, they need to improve the performance of their core business and catch up with digital companies in flexibility and responsiveness. Only by doing this they can compete with digital invaders in their field.

Stay connected!